March 13, 2024

If you’re a property investor, you’ll know that investing in buy-to-let means you’ll face additional costs in respect of property taxes, be it Land & Building Transaction Tax (LBTT) for Scotland or Stamp Duty Land Tax (SDLT) for the rest of the UK.

Given the importance of the private rented sector (PRS) to the UK housing market such additional taxes can be a discouragement to investment, so this seems rather counterintuitive.

However, if you buy a number of properties in a single (or linked) transaction, some relief is available, to encourage investment in property. But, probably as of 01 June 2024, only in Scotland. Confusing isn’t it?

Regardless, this is the world we live in. How, therefore, do you maximise your commercial benefit whilst minimising the cost? As buy-to-let property professionals, we’re going to discuss the best ways to approach this conundrum.

Multiple Dwellings Relief (MDR) – what it is and how to qualify

What is multiple dwellings relief in the UK and what is its purpose? Scottish Revenue describe it thus:

“Multiple dwellings relief (MDR) is available on most transactions that involve the purchase of more than one dwelling in a single transaction or in a series of linked transactions.The relief ensures the buyer does not pay LBTT at a higher rate than if bought separately and lower rate bands would have applied.”

Whilst this definition applies specifically to transactions in Scotland, the principal is the same north and south of the border.

It also succinctly explains why the relief is available; to ensure that a transaction involving multiple dwellings, which will almost always involve a higher purchase price is taxed fairly compared to a series of single transactions.

In that respect it is intended to encourage property investment, but only insofar as it levels the playing field.

Ok, that’s MDR in principle, how does it work in practice and does location – Scotland vs the rest of the UK matter?

MDR in Scotland

If you’re purchasing property in Scotland with a view to renting it out, you face LBTT and usually Additional Dwelling Supplement (ADS). ADS is currently tagged at 6% of the purchase price of the property.

The instance where ADS is not payable is when the property is valued at less than £40,000 or if you get MDR on ADS by buying six or more properties in one transaction.

It’s complicated but I should point out that you can still get a form of MDR when buying less than six properties but you’ll not get relief from ADS, so it’s potentially not as much of a saving.

I’m NOT an accountant but I do spend time calculating the rough MDR on Scottish property portfolios. And I can tell you that MDR is figured out as a combination of residential and commercial rates, either including or not including ADS.

Scottish Revenue lays out a series of steps for calculating the amount of MDR available when purchasing property in Scotland, although we would much rather they had developed a calculator!

They do show worked examples, but we’ll understand if you need to lie down in a darkened room afterwards. Specifically, have a look at MDR+ADS (6+ Dwellings).

Please note that MDR in Scotland will be under serious review since the 2024 Budget that announced it’s being abolished in England. We’ll do our best to update this blog accordingly.

Top Tip: We’ll simply note that our oft-repeated advice about the importance of a good accountant may well pay dividends here!

MDR in England

As mentioned, MDR is to be abolished in England and Northern Ireland from 01 June 2024. So, in truth, I’m not sure it’s worth discussing what it was and how it worked!

Some of the other differences in property purchase include;

- MDR in England could be gained on less than six properties

- The additional dwelling supplement (ADS) is referred to as Higher Rates on Additional Dwellings (HRAD).

Here is a good article on HRAD – 3% Stamp Duty Land Tax on Second Homes.

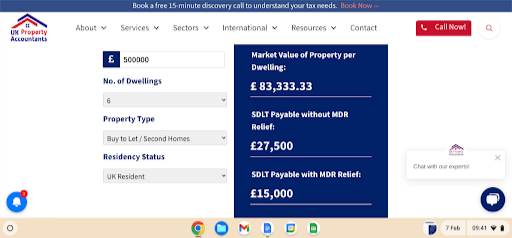

Fortunately, unlike Scotland, we did find a calculator which is useful for property investors, so a big thanks to UK Property Accountants.

The nice thing about this calculator is that it clearly shows the effect of claiming MDR on the suggested transaction, making it easy to see whether or not there is a benefit. Even though it will not be relevant from 01 June 2024.

Multiple Dwellings Relief – is it always a benefit?

Now, this may seem like an odd question to ask, but it’s relevant. Given that the aim of multiple dwellings relief in the UK is to level the playing field in respect of LBTT/SDLT when a number of properties are bought, the answer isn’t always ‘yes’.

The image above goes some way to explaining why. Although it is less likely in the current market, if the average value of the properties involved falls to, or below, the lower limit for land tax, there will be no benefit to claiming.

Indeed, any claim may be rejected as not applicable.

Another interesting issue is raised by Mishcon deReya, solicitors, and that is the danger of scams. The linked article is a quick read, but the short version is beware of anyone who approaches you claiming that you could make money by claiming MDR.

At the very least you’ll lose some money to ‘fees’, at worst you could end up owing HMRC money. HMRC, being HMRC, might also levy interest and a fine on ‘incorrect refund claims’.

Trust your solicitors and accountants before strangers who suddenly have your best interests at heart…

Advice from the property pros

Unlike the much lamented MIRAS (Mortgage Interest Relief At Source) scheme, multiple dwellings relief in the UK doesn’t feel like such a benefit to property investors.

However, as the examples shown demonstrate, you can achieve substantial savings when purchasing multiple properties for let. Unlike MIRAS, this is only a benefit to those who are expanding their property portfolio.

How much you can save depends on factors too numerous to explore exhaustively. As to whether or not MDR favours purchases north or south of the border, UK and International Tax Planning are quite clear on their thoughts.

In part this northern advantage seems to hinge on the fact that as mentioned previously, ADS in Scotland is an additional, separate tax, whereas elsewhere in the UK it’s common to encounter higher rates of Land Tax.

In summary…

Multiple dwellings relief isn’t a subject which is likely to spawn any misty-eyed conversations of an evening over a nice bottle of red wine. However – if you are expanding your portfolio, it can make a substantial difference to your tax liability.

Since the current market seems to favour those who can invest in multiple properties, this makes the relief especially relevant. We have often written of the potential advantages of a property portfolio, this is another.

Whether you are ready to make a substantial investment in the property market and your future, or if you are still mulling over buying a single buy-to-let, we can help advise and guide you through the hoops and hurdles.

Pick up the phone, drop us an email and let’s have a conversation that could change your life.

Written by Chris Wood, MD & Founder of Portolio

Get in touch on 07812 164 842 or email [email protected]

Comments